We spent $6,600 on a 3-bed to 4-bed conversion. Here’s what happened.

Converting a 3-bedroom house into a 4-bedroom is one of the least talked-about value-add strategies in property investment. And for good reason – when it works, the numbers are hard to argue with.

But the gap between “this could work” and “this actually worked” is bigger than most investors think.

So instead of theory, let’s start with a real deal.

The deal: $6,600 that created $50,000

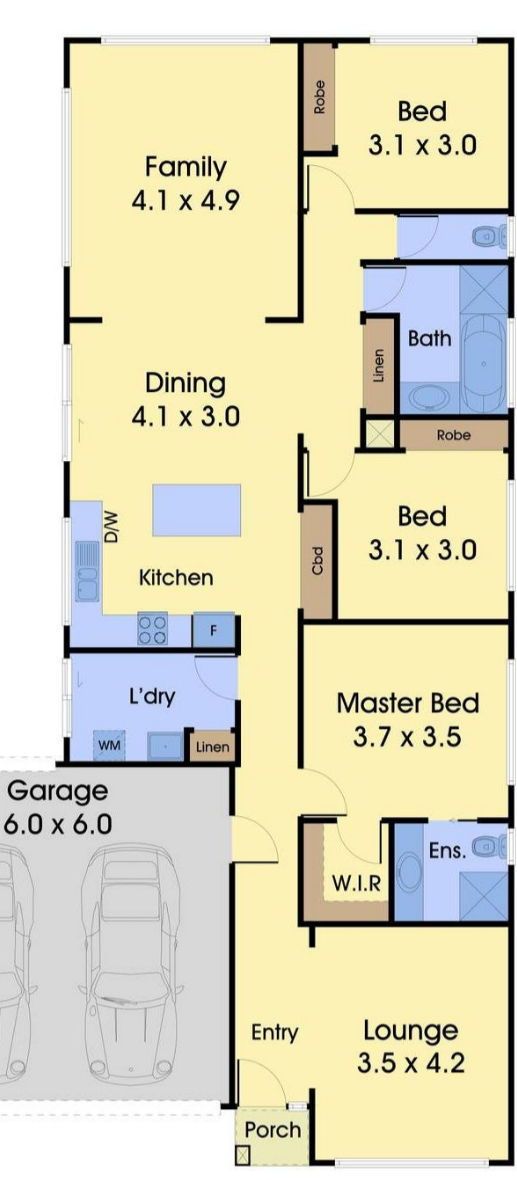

We bought a client a 3-bedroom property for $750,000. The house was 158 square metres – a decent-sized family home with an open-plan kitchen, family, and dining area at the back, and a separate formal lounge at the front.

That lounge was 3.5 by 4.2 metres. Nearly 15 square metres of space that, in the context of an investment property, wasn’t really earning its keep.

We gave the client two options to consider:

Option 1: Extend a wall and add a door – no wardrobe. Keep it as a multi-purpose room that could function as either an extra bedroom or a second living area, depending on the tenant.

Option 2: Add a wardrobe and commit to a proper fourth bedroom.

The client went with Option 2. Wall extension, door, built-in wardrobe, fresh paint, light and power point. Total cost: $6,600.

The result?

Property revalued at $800,000. That’s $50,000 in instant equity on a $6,600 spend.

Rent increased by $40 per week – that’s $2,080 per year, every year, for the life of the investment.

On paper, that’s a 7.6x return on cost for the equity uplift alone, plus an extra annual yield on the conversion spend from the rental increase.

Pretty hard to find a renovation project that delivers that kind of return for under seven grand.

Why this conversion worked

The numbers are impressive. But the reason this worked wasn’t the conversion itself – it was the decision-making behind it.

The floor plan supported it. At 158 square metres, the house had enough space to absorb a conversion without the rest of the layout suffering. The family and dining area at the back was generous – 4.1 by 4.9 for the family room plus 4.1 by 3.0 for dining. Taking the lounge didn’t leave the house feeling cramped.

The lounge was the right candidate. At nearly 15 square metres, it was large enough to become a proper bedroom without feeling like a cupboard. It already had natural light and ventilation. It already met the physical requirements of a habitable room.

The area supported 4-bedroom demand. The suburb’s tenant and buyer profile favoured larger homes. A fourth bedroom moved the property into a higher-demand bracket, both for rent and for future resale.

The spend was proportionate. $6,600 against a $750,000 purchase is less than 1% of the property value. The risk was minimal, and the upside was asymmetric.

Every one of those factors had to be true for this to work. Remove any one, and the conversion stops making sense.

When a 3-bed to 4-bed conversion doesn’t work

This is the part that most property content skips. Everyone wants to tell you about the upside. Nobody wants to talk about the houses where a conversion makes things worse.

The house is too small

Take a 130 square metre house with two small separate living areas. You could technically turn one into a bedroom. But now both remaining spaces feel tight, the layout doesn’t flow, and you’ve created a 4-bedroom house that feels worse to live in than the 3-bedroom version.

An extra bedroom only adds value if the rest of the house still works. If you’re robbing one room to pay another, you haven’t created value – you’ve just moved it around.

The wrong room gets converted

Not every living space is a good conversion candidate. A room at the centre of the house with no external wall? No natural light. A narrow room that can only fit a single bed? Not a credible bedroom in a family home.

The room has to work as a bedroom in practice, not just on a floor plan annotation. Tenants and buyers can feel the difference between a real room and a box you’ve called one.

The area doesn’t support it

If the local market is dominated by young couples or downsizers who want open-plan living and low maintenance, adding a fourth bedroom at the cost of living space is solving a problem that doesn’t exist.

Conversely, in suburbs with strong demand from larger families or shared households, a 4-bedroom property can command significantly more rent and a higher sale price. The strategy has to match the market.

The room nobody thinks about losing

Here’s one that trips up a lot of investors who are purely focused on bedroom count.

Some families – for cultural, religious, or lifestyle reasons – genuinely need two separate living spaces. A formal lounge and a family room aren’t a luxury for them. They’re a practical requirement – for hosting, for prayer, for separating adults and children, for multi-generational living.

If you convert that second living space into a bedroom, you’ve just excluded a significant segment of the rental and buyer market. In some suburbs, that’s the segment that would have paid the highest rent.

This is why understanding the demographic profile of the area isn’t optional. It’s not a nice-to-have. It’s the difference between adding value and destroying demand.

What the building code actually requires

You can call a room whatever you like on a listing. But for it to legally qualify as a bedroom, it needs to meet specific standards under the National Construction Code (NCC).

The key requirements include:

→ Minimum floor area. While there’s no single national figure, the general benchmark is around 6.5 square metres for a single bedroom. Anything smaller starts to fall below what valuers and compliance inspectors will accept.

→ Natural light. The room needs a window. Not a borrowed light from another room, not a skylight in a hallway – a window to the outside.

→ Ventilation. Adequate airflow, typically via an openable window. Mechanical ventilation alone generally doesn’t satisfy the requirement for a habitable room.

→ Egress. In the event of an emergency, occupants need a compliant exit path. This is particularly relevant if the conversion involves altering the room’s access to corridors or external exits.

If the room doesn’t tick every one of these boxes, it’s not a bedroom in the eyes of anyone who matters – valuers, lenders, insurers, or the tenancy tribunal.

It’s also worth checking whether the conversion requires council approval. In some jurisdictions, adding a bedroom can trigger a development application or a complying development certificate, particularly if it changes the building’s occupancy classification. Skipping this step can create compliance issues that cost far more to fix than the original conversion.

Why your bank might not care about your new bedroom

This is the one that really stings.

You’ve done the conversion. It looks great. The tenant’s paying more rent. You apply to refinance based on the higher valuation – and the bank valuer walks in, takes one look, and still calls it a 3-bedroom.

It happens more often than you’d think.

Bank valuers assess what a room legally is, not what you’re marketing it as. If the room doesn’t meet building code, or if the room simply doesn’t present as a credible bedroom – they won’t count it.

That means your expected equity uplift doesn’t materialise. Your refinancing plan stalls. And the money you spent on the conversion delivers zero return in the lender’s eyes.

In our case study, the conversion worked because the room already had natural light, ventilation, proper access, and enough floor area to function as a genuine bedroom. The wardrobe and wall simply formalised what the space could already support.

That’s the difference between a conversion that creates equity and one that creates a fiction.

The smarter play – dual-purpose design

Our client went with a full bedroom conversion – and for their property and market, it was the right call. But it’s not always the right call.

If there’s any doubt about whether the area’s market prefers bedrooms or living space, the smart play is to design the conversion so the room works as either.

→ Sliding or cavity doors instead of a fixed wall – so the room can be closed off as a bedroom or opened up as a living area

→ Built-in joinery that doubles as a wardrobe or an entertainment unit depending on configuration

→ Smart positioning so the room integrates with the rest of the house in both layouts

This way, a family that needs four bedrooms gets what they want. A family that needs two living spaces also gets what they want. You’re not betting on one market – you’re capturing both.

It costs slightly more upfront, but it protects your property’s appeal across a wider tenant and buyer pool. That’s not a renovation decision. That’s a strategic one.

The checklist before you convert

Before committing to a 3-bed to 4-bed conversion, run through every one of these:

1. Floor plan suitability. Is the house large enough to absorb a conversion without making the remaining spaces feel cramped?

2. Room quality. Does the room you’re converting have natural light, ventilation, and enough floor area to function as a real bedroom?

3. Building code compliance. Does the room meet NCC requirements for size, light, ventilation, and egress?

4. Council requirements. Does the conversion need DA approval or a complying development certificate in your jurisdiction?

5. Market demand. Does the suburb’s buyer and tenant profile favour a 4-bed over a well-designed 3-bed with two living areas?

6. Demographic awareness. Are there cultural, religious, or lifestyle factors in the area that make a second living space more valuable than an extra bedroom?

7. Dual-purpose potential. Can the conversion be designed so the space works both ways?

8. Cost vs. uplift. Does the spend justify the expected increase in value and rent? Is the return asymmetric in your favour?

9. Bank valuation reality. Will a valuer actually recognise the room as a bedroom – and will the bank lend against the higher figure?

If you can’t confidently answer every one of those, you’re not ready to convert. And if you’re guessing on more than two, you probably need someone who’s done this before to walk through it with you.

Strategy without context is just guesswork

The 3-bed to 4-bed conversion is one of the most powerful low-cost plays in property investment. Our client turned $6,600 into $50,000 in equity and an extra $2,080 a year in rent. That’s a result most full-scale renovations can’t touch.

But it worked because the property, the floor plan, the room, and the market all supported it. Remove any one of those, and the same strategy becomes an expensive way to make a house worse.

Every property is different. Every suburb has its own demand profile. And every conversion decision should be made with the specific property in front of you – not a generic playbook from a YouTube video.

That’s what a good buyer’s agent does. Not just finding the property – but knowing what to do with it once you’ve got it. And, just as importantly, knowing when to leave it alone.